Dispute regarding the Claimant’s acceptance of the Respondent’s return and the correct return amount based on inspection results and current market value.

The Fruit and Vegetable Dispute Resolution Corporation (DRC) has developed a series of articles summarizing past arbitration decisions. These articles will help members understand how the DRC Dispute Rules and Standards (R&S) apply in a dispute.

The DRC Dispute R&S states that all DRC arbitrations are private and confidential. As such, the names of all parties, including the Arbitrator and companies, are not included. A reminder that the DRC’s sole role is as administrator of the arbitration process; the DRC does not participate in any hearings. Therefore, this summary is based solely on the Arbitrator’s written decision and may not reflect important information shared with the Arbitrator through written briefs or verbal testimony.

ABSTRACT

This arbitration decision involves a dispute between a U.S.-based Claimant (seller) in Pennsylvania and a Canada-based Respondent (buyer) in Montreal over two shipments of Colossal Yellow Onions. The key issues were whether the Claimant accepted the Respondent’s return offer and what constituted an appropriate settlement based on inspection results and market value. According to the findings and the DRC Rules, the Arbitrator concluded that there was sufficient evidence to show that the Claimant accepted the return amount offered by the Respondent for only one of the two shipments. For the second shipment, however, the Arbitrator found that the Respondent did not provide enough evidence to justify the proposed return. Additionally, the inspection results did not support the amount offered for the return of the second shipment.

Below is a concise analysis of the case, its implications, and key takeaways for similar international commercial disputes.

CASE: DRC FILE #20535 – PARTIES DOMICILED – UNITED STATES AND CANADA

SUMMARY OF FACTS:

The Claimant, based in Pennsylvania, sold two loads of Colossal Yellow Onions to the Respondent located in Montreal.

The first load consisted of 850 bags, each weighing 50 lbs, sold FOB Idaho for USD 7.25 (invoice #50432 or PO 60298). The product was shipped on December 11 and arrived on December 15.

A CFIA inspection was requested and performed on December 16, revealing 9% total condition defects. This included 1% cuts, 2% translucent scales, 1% watery scales, and 5% decay.

The second load also contained 850 bags of 50 lbs Colossal Yellow Onions, sold FOB Idaho for USD 8.00 (invoice #50433 or PO #60308). This product was shipped on December 18 and arrived on December 20.

A CFIA inspection was requested on December 21 and performed on December 23, showing 10% total condition defect comprising 3% translucent scales and 7% decay.

After the inspections were completed, the Respondent emailed the results to the Claimant’s sales representative. On December 23, the Claimant replied, asking if the Respondent would like to repack the product and whether they were interested in settling the matter. The Respondent responded the same day, stating that they could only settle after selling the product. However, due to the significant decay (as high as 25%), they believed they could only recover the cost of freight. The Respondent followed up with a phone call to emphasize the limited resources available for selling the product. It was suggested again that the Claimant take back the product to minimize losses for the grower.

On December 27, the Claimant emailed the Respondent to inquire about the returns for the onions.

On December 31, the Respondent replied, indicating that there would be a remittance of USD 1.00 per bag, all-inclusive, along with revised invoices for both loads, allowing the Claimant to issue payment.

On January 8, the Claimant emailed the Respondent, advising that given the inspections, market value, and damages, the return should be between USD 5.00 and USD 6.00 FOB, and they would likely not accept anything less. The Respondent replied on the same day, stating that the product was out of grade and was sold to minimize losses at the best possible price, considering the percentage of decay present in both loads. They confirmed that the USD 1.00 payment had been made in full and that no additional funds would be provided.

On January 23, the Respondent received an email from the Claimant stating that the grower had accepted a return of USD 1.00 per bag for PO#60308 and had created a credit memo, which was included in that email.

SUMMARY OF ARBITRATOR’S ANALYSIS AND REASONING:

After considering all of the arguments and submissions from both parties, the Arbitrator focused only on the relevant points that influenced their conclusions and the resolution of the dispute. Any facts or arguments that were not addressed in the Arbitrator’s reasoning did not affect the conclusion of their Arbitral Award.

- Both Invoice #50432 and Invoice #50433 pertain to sales transactions. Since there is no other written agreement between the parties, the DRC rules are applicable, as both parties were members of the DRC when the dispute arose.

- It appears that the Claimant was acting as a commission merchant on behalf of a grower regarding each of the sales in question.

- There is no evidence indicating that the parties agreed on a specific grade standard. Therefore, the DRC’s Good Arrival Standards apply. Under these standards, the allowable decay for onions is 4%, and the product in question exceeded this tolerance level.

- Specifically concerning Invoice #50433/PO #60308, the evidence shows that on January 23, 2020, the parties agreed to a return of USD 1.00 per bag.

- Regarding Invoice #50432/PO #60298, there is no evidence that the parties reached an agreement on a reduced price, nor is there any indication that the level of decay merited a price reduction to USD 1.00 per bag. The decay was 7%, “mostly also showing mold.”

- It is the Respondent’s responsibility to provide evidence to support its returns. However, the Respondent did not supply any accounting for the Arbitrator to evaluate the sales, timing, and prices.

- As a consequence, the Arbitrator rejected the Respondent’s return on the products corresponding to Invoice #50432/PO #60298.

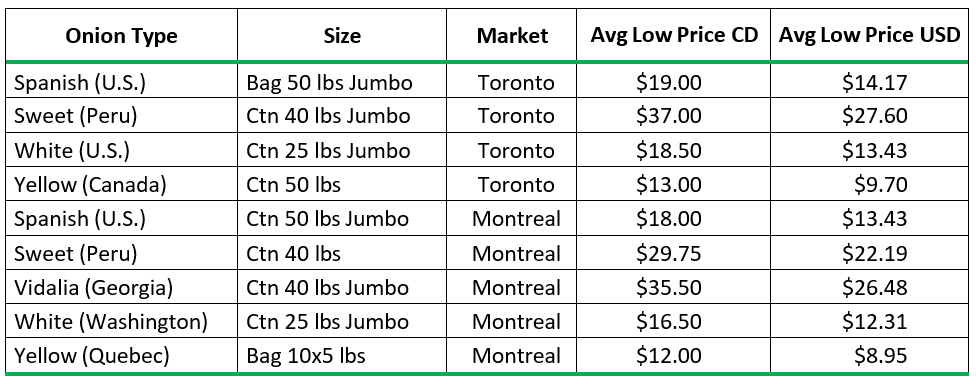

- According to the Agriculture and Agri-Food Canada website, the prices for the week of December 16, 2019, for comparable conventional onions were:

- The Claimant’s damages claim in this arbitration is USD 6.50 FOB per bag (less than the USD 7.25 original price), which is well below the market prices available for a comparable product at No. 1 grade in Canada in the corresponding time frame.

- Consequently, the total price for Invoice #50432/PO #60298 is determined to be USD 5,525.00. Since USD 850.00 has already been paid, a balance of USD 4,675 is still owed by the Respondent.

- Further, Claimant’s invoices provide that the buyer shall pay all costs of collection. Accordingly, the Respondent is required to pay to the Claimant the USD 600 DRC filing fee.

ARBITRATOR’S SUMMARY DECISION:

Based on the Summary of Arbitrator’s Analysis and Reasoning, the Arbitrator makes the following decisions:

- Claimant’s claim regarding Invoice #50433 / PO #60308 is DISMISSED.

- The Respondent did not provide an accounting or proof of claim for Invoice #50432 / PO #60298.

- The Respondent failed to make the payment for Invoice #50432 / PO #60298.

- Respondent must pay Claimant USD 4,675.00 in general damages and USD 600.00 for the DRC filing fee by August 29, 2020.

- All other requests that were not granted are DISMISSED.

DRC COMMENTS:

In the produce industry, if a buyer decides to claim damages after receiving a product in a deteriorated condition, it is the buyer’s responsibility to explain how they arrived at their decision for the return. While an itemized account of sales is only required in consignment transactions, providing an account of sales is the most common method when claiming damages resulting from a breach of contract or a product received in deteriorated condition.

When submitting an account of sales, it is advisable to present an itemized account of sales. This should include the date, amount, and price for each sale related to the load in question, after deducting expenses such as freight costs, inspections, brokerage fees, and any additional expenses agreed upon by both parties. An itemized account of sales not only illustrates net returns but also demonstrates whether the product was moved promptly.

If an account of sales is unavailable, be aware that there are alternative methods used to assess the fair value of the product. One approach may involve reducing the invoice value based on the percentage of defects identified in the federal inspection, although this may not always accurately reflect actual losses.

ADDITIONAL RESOURCES:

To access the full redacted arbitration decision, click here.

Receiver Duties:

Articles: